MARKET UPDATE: December 2020

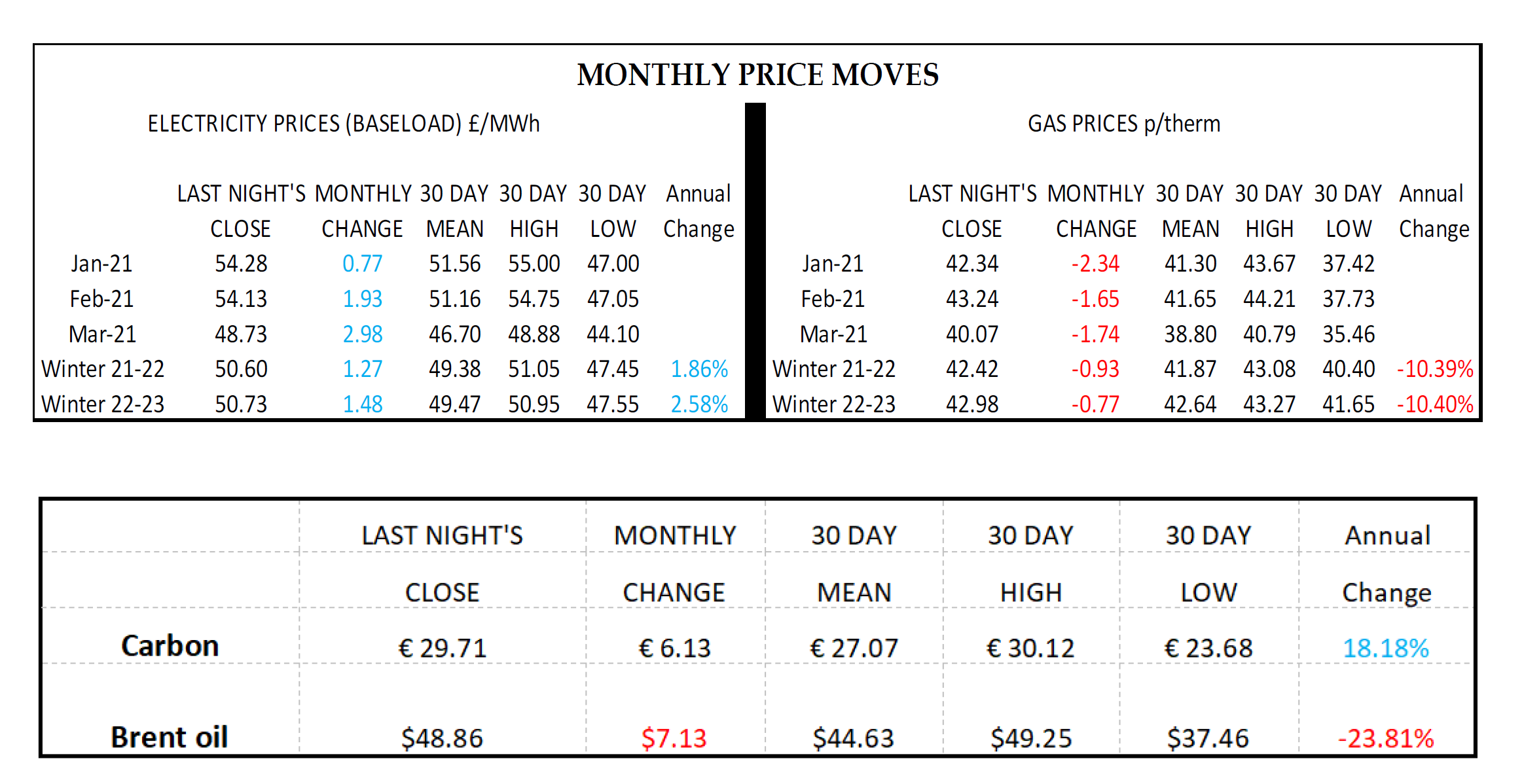

Market review data for December 2020 provided by West Mercia Energy

Market review data for December 2020 provided by West Mercia Energy

LOOKING AHEAD PRICES WILL BE INFLUENCED BY:

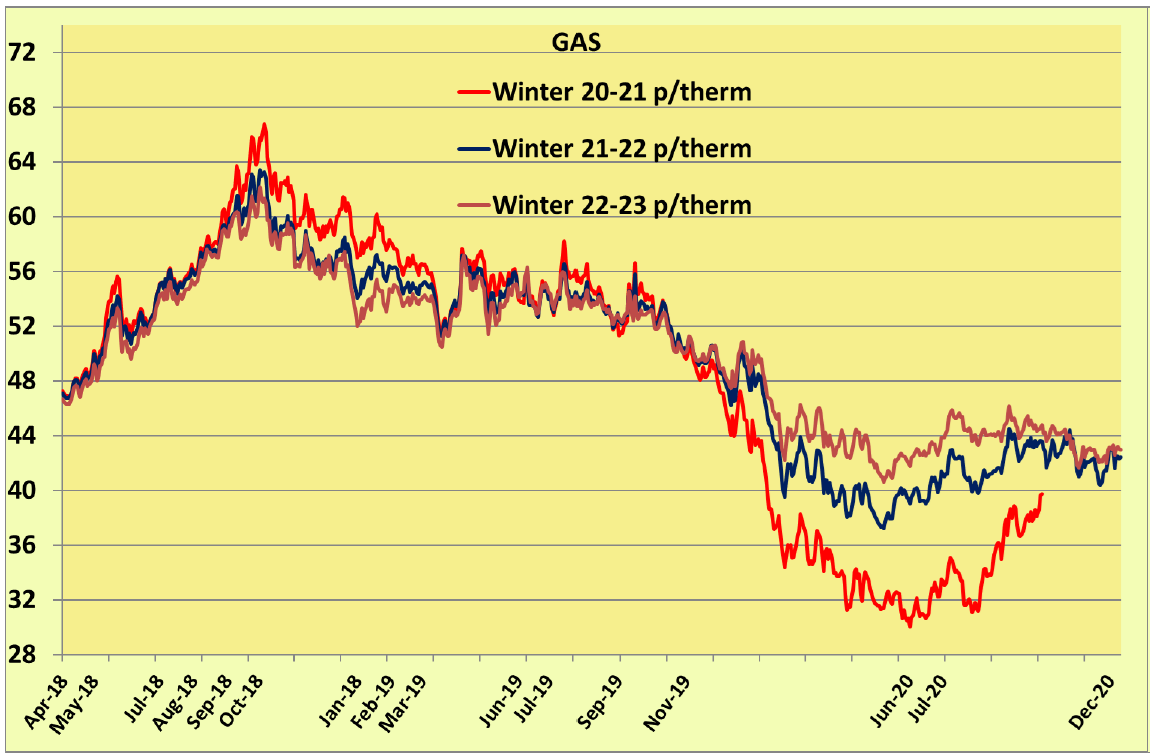

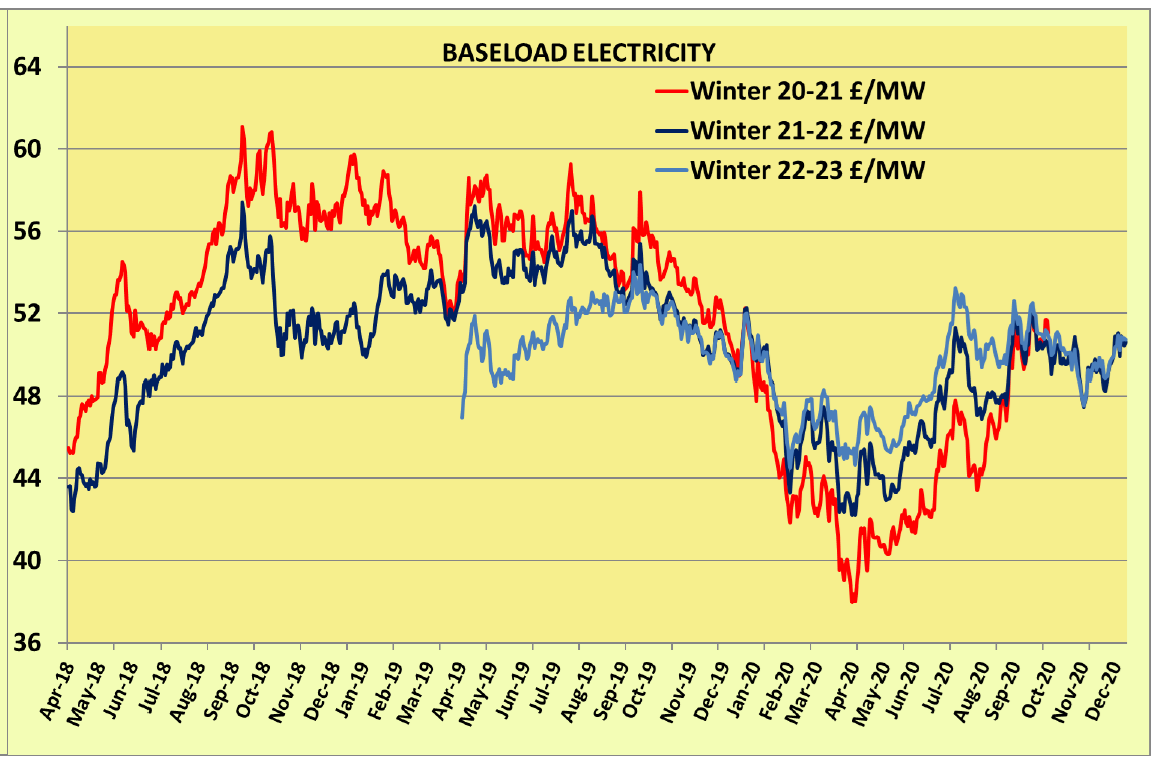

Gas and electricity prices have moved in opposite directions over the last month, with gas prices losing value as a result of a relaxation in supply concerns, whilst rising carbon prices have seen corresponding rises in electricity prices. Both gas and electricity prices remain volatile.

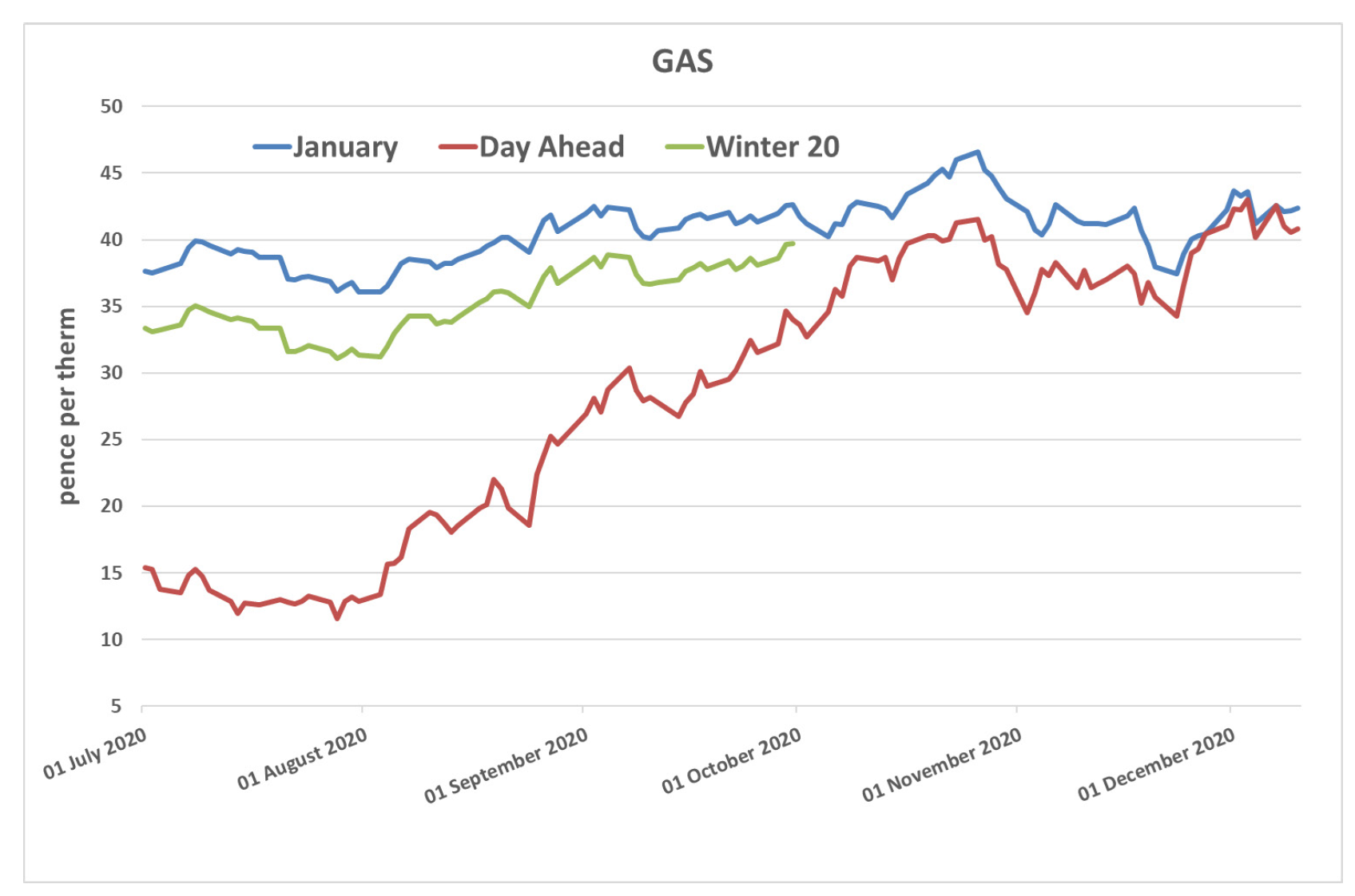

The relaxation of these supply concerns can be seen in the graph on the right which shows how January gas prices have fallen from their highs of late October. Day Ahead gas prices have continued to increase as would be expected at this time of year with increases in demand, and have now converged with January gas prices. This emphasises the importance of Day Ahead gas prices in determining gas prices from January onwards. Low wind generation coupled with cold weather has seen very high electricity Day Ahead prices so far in December and this has leant some support to prices from January onwards.

One reason for this relaxation in supply concerns for gas has been an increase in LNG flows as a result of an influx of cargoes during November and early December.

As can be seen from the graph alongside, LNG flows are approaching the highs that we saw this time last year. This increase in shipments has predominantly been as a result of an increase in US cargoes, and has helped to offset higher Asian gas prices which has attracted all available LNG shipments from Qatar away from Europe. To put the importance of LNG into context, today it is accounting for approximately 25% of supply. The ongoing availability of LNG will be a major factor in short term gas prices.

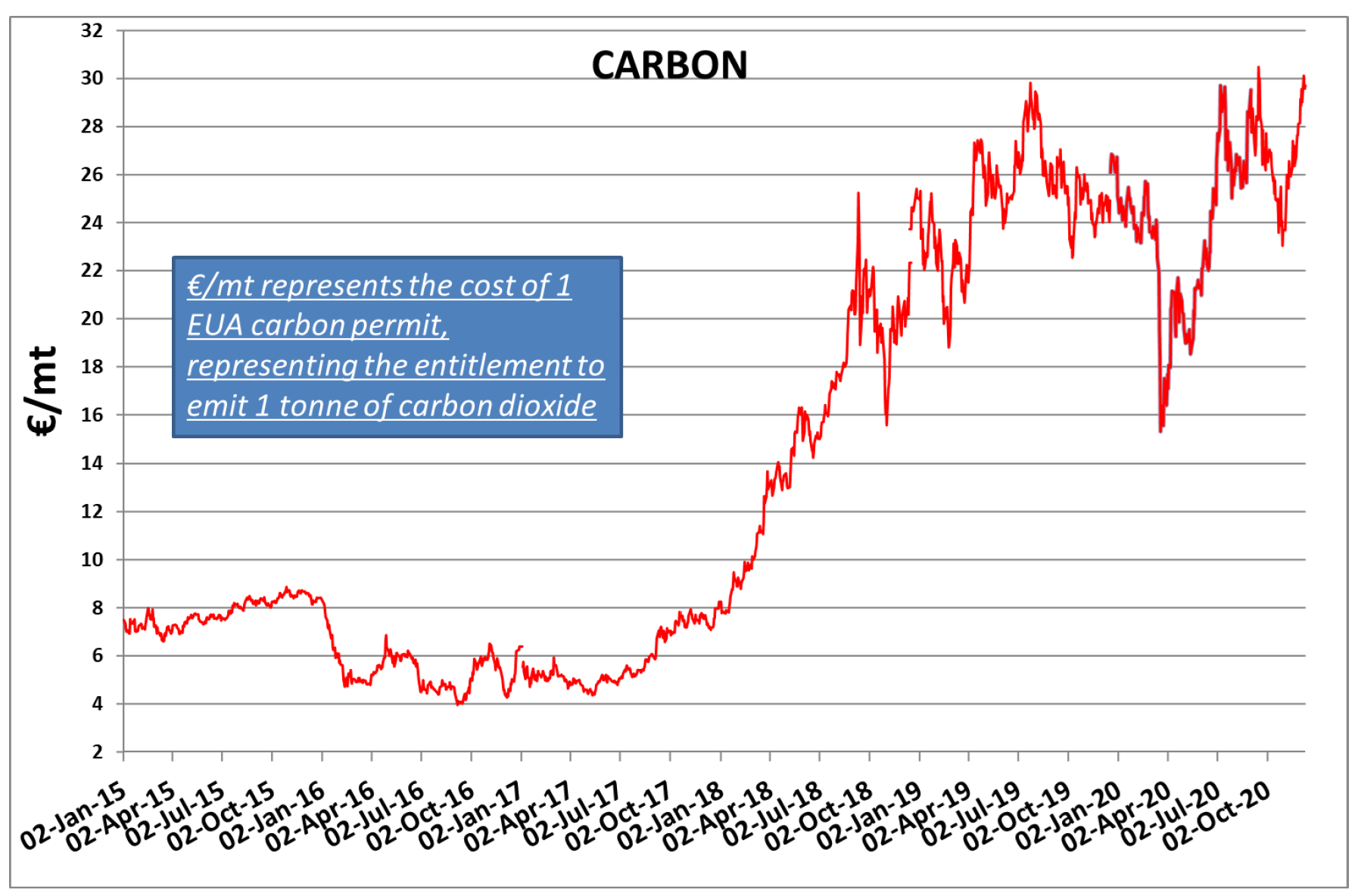

In contrast to gas prices, electricity prices have increased in the last month, mainly as a result of an increase in carbon prices which are threatening once again to break through the key €30 per tonne resistance level. This increase is partly due to speculation regarding the outcome of a EU council

meeting taking place currently which could announce reductions in the 2030 emissions target.

Further support for carbon prices has come from delays in free allowance issuance and the 2021 auction schedule announced by the European Commission. Carbon prices represent a tax on electricity generation and therefore any move in carbon prices is likely to have a commensurate

impact on electricity prices.

Brexit negotiations appear to be entering a crucial final stage with the possibility of a ‘No Deal’ Brexit remaining high. In that eventuality there could be an impact on gas and electricity prices, mainly as a result of an anticipated fall in the value of the pound in relation to the euro which would result in higher import prices. There could also be an impact on carbon prices depending on how the UK trades after leaving the EU. In addition, if the UK also left the Internal Energy Market with the result of cross border tariff’s being imposed (both ways) then the UK and remaining EU nations could see a rise in wholesale energy costs and price volatility during cold weather or network constrained circumstances. The view has always been that security of supply will be maintained, but this may come at a price.

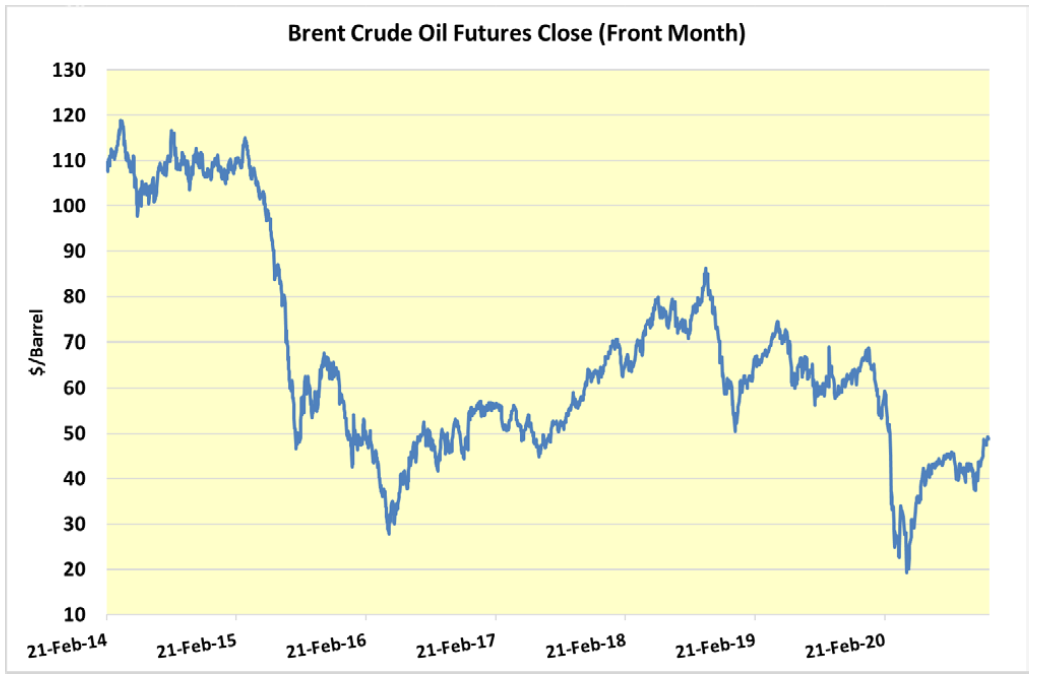

Oil prices have increased over the last month, partly as a result of OPEC supply cuts which have been extended into 2021, and partly due to the news of the successful trials and roll-out of the Covid-19 vaccines which offer the prospect of a recovery in oil demand in 2021. This increase in oil prices has offered support to gas prices because gas contracts index-linked to oil prices are still relatively common in Europe.

SUMMARY

Gas and electricity prices are likely to remain volatile as we await the result of key Brexit negotiations and the outcome of the EU Council meeting discussing the future of carbon emission reduction targets. Asian gas prices and European weather forecasts are also likely to have an influence on short term markets, as will Covid-19 and the potential for further lock-down measures before the end of the winter and the longer term impact on the European and Global economies. In the shorter term, possible strike action by French nuclear production workers could also impact on the availability of French electricity imports and in turn impact on UK electricity prices.